DOWNLOAD

DATE

MEET THE AUTHORS

Contact

1. Fiber (FTTH/B) investments are more common now than ever before

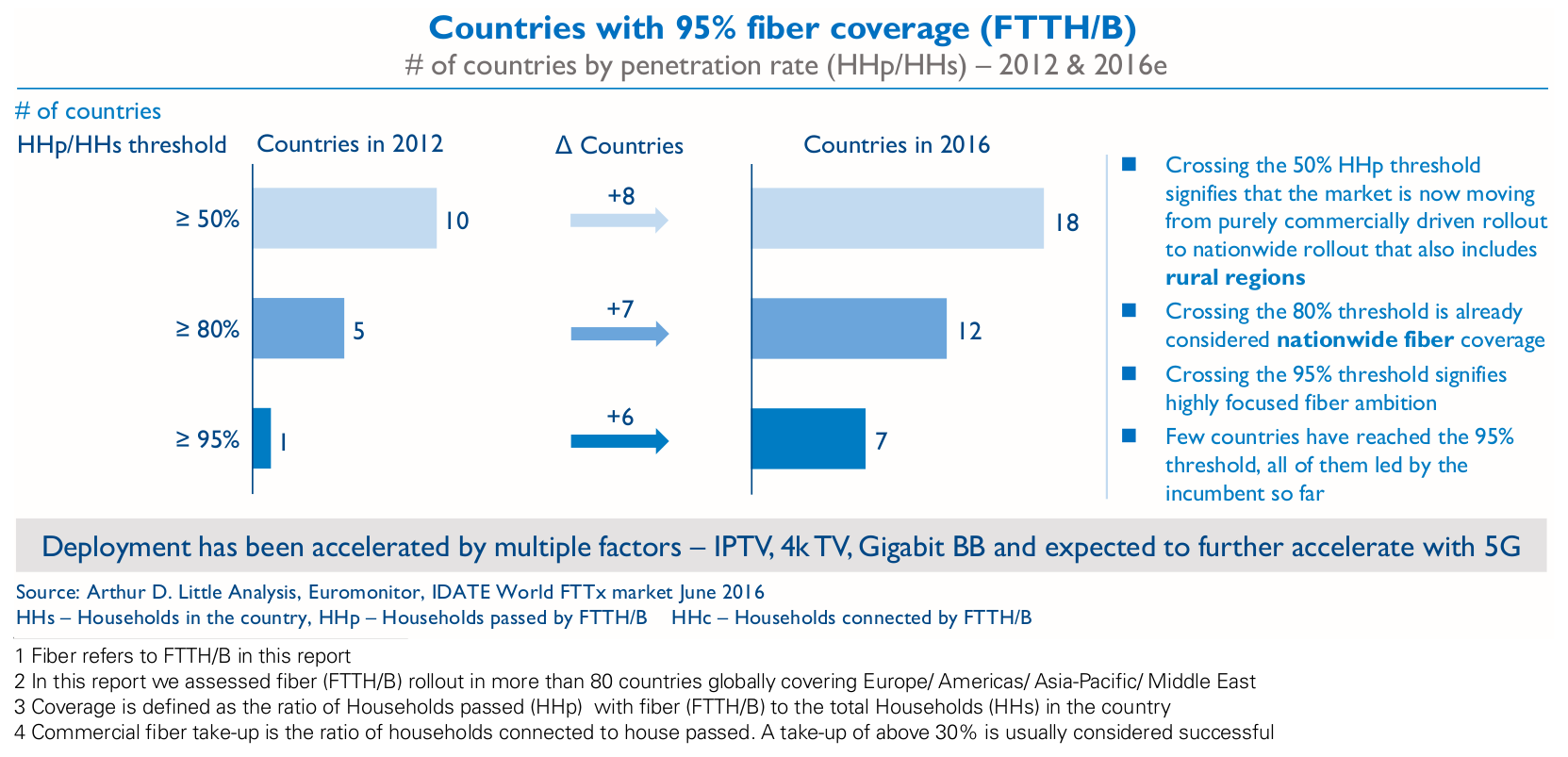

Fiber1 investments have become more common now than at any point in the past. Since we published the previous version of our Global Fiber Report in 2010 and 2013, the number of countries2 with more than 95% fiber coverage3 has increased from just one (in 2012) to seven countries (in 2016) and the number of households passed with fiber has increased by 20% percentage points since 2013 globally.

Successful fiber rollout is independent of the size of the country or its GDP per capita. Fiber rollout has been successful in both in smaller high GDP countries like Singapore & Qatar, in medium size high GDP countries like Spain, Portugal and New Zealand, as well as a large but lower GDP country like China. In all these countries fiber rollout was primarily driven by the incumbent, with or without government support and in some cases, the challenger TelCo has also actively rolled out fiber. In the first edition of this ‘Global FTTH Report – Double squeeze of the incumbent’ we highlighted that the incumbent was getting squeezed by CableCos and alternative operators in order to roll out next generation broadband. In this report we observe the comeback of the telecom incumbent – incumbents are taking the lead (in some cases also the challenger TelCos) in countries that are successfully rolling out nationwide fiber.

In countries that have seen slow rollout, the incumbent did not, or is still not taking the lead. We have seen fiber rollout programs being paused in countries Australia & USA. Some other countries like Austria, Germany & UK have yet to start nationwide fiber rollout programs. It is interesting to note that irrespective of the size of the country or its GDP per capita, a large developing country such as China is successfully rolling out fiber, while India has not yet started. Similarly a high GDP country like Spain already has more than 80% fiber coverage, while comparable Germany is yet to start nationwide fiber deployment.

The incumbent driven fiber rollout model is becoming the most common rollout model for fiber. In the previous edition of this report, we had introduced five fiber rollout models, and had predicted that the best model is when the incumbent takes the lead with graded government support. We observe that this model is still the most successful and common model used.

Commercial4 take-up of fiber has followed rollout, albeit sometimes with delays. We have not yet seen an example of low fiber take-up following rollout. Some countries like Singapore has seen successful take-up, but with a gap of 3-4 years after rollout, while other countries like Qatar has seen faster take-up success within a span of 2 years after rollout. In most cases the main driver for success of take-up is migration of customers from legacy technologies to fiber, while competition and launch of innovative products further aids it. In a dozen countries with strong fiber rollout programs in place, innovative products like gigabit broadband and 4k TV have been successfully launched.

Unlock a Powerful Difference

RELATED INFORMATION

Arthur D. Little: Decisive National Fiber strategies needed to boost future economic growth

The telecom industry, governments and regulators need to move decisively to fiber in order to support future economic growth, states Arthur D. Little (ADL) in its new report, “National Fiber…

Arthur D. Little: Failures in telecom policy and regulation could hamper economic growth in Europe

The telecom industry, governments and regulators need to move decisively to fiber in order to support future economic growth, states Arthur D. Little in its new report, “National Fiber Strategies:…

Arthur D. Little identifies cable infrastructure as a competitive next generation platform especially in the current financial crunch

In many countries, cable infrastructures have been the key enabler for multimedia services, and some leading players are already winning the broadband race with higher penetration within their…